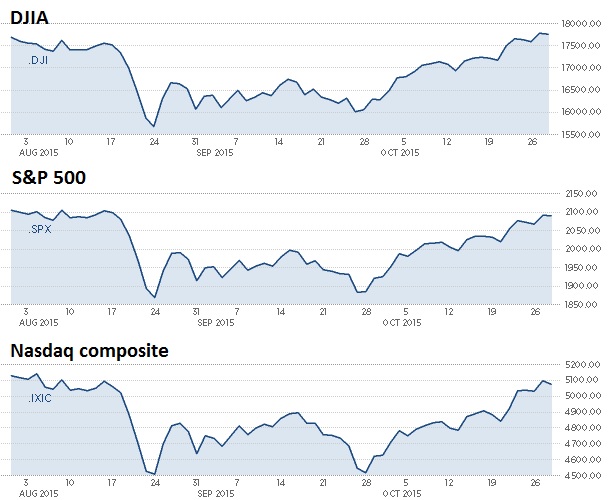

Month In Review: Bullish Month On Wall Street

Stocks Rally On More Easy Money

Stocks soared in October and enjoyed one of their largest monthly gains in years! As a quick review, the bulls regained control of the market on Fri 10/2/15 after September’s weaker than expected jobs report was announced (additionally, Aug’s and July’s jobs reports were both revised lower). That was a pivotal day because it changed the market’s perception and basically eliminated the chance the Fed will rates anytime soon. For months, we have argued that, “Wall Street is ready for a rate hike but Main Street clearly is not. So the easy money trade is alive and well (for now).” Fundamentally, that is the primary driver of this entire/aging bull market and trumps the weak action we continue to see from Main Street (both on the earnings and economic front). Technically, the bulls defended Aug’s low at the end of Sep/early Oct and helped the benchmark S&P 500 form a bullish double bottom pattern “W.” This powerful pattern looks very similar to the Nasdaq in 1998 (before it soared into the March 2000 high). After the August lows were defended and the bulls knew the Fed would not be able to raise rates at their meeting in Oct, the market soared. Later in the month, the Fed did not raise rates and the European Central Bank added more easy money into the mix when they said they are ready to increase and extend QE (print more money), if needed. In the short term, the market is extended to the upside and due for a little pullback here to digest the recent and strong rally off support. We also want to note that over the past four weeks, the S&P 500 soared a whopping +11% which is not an insignificant sum. Remember, in “normal” (non QE) days, a 10% gain for the entire year was considered healthy. The big negative divergence remains the small-cap Russell 2000 and the fact that it is under performing on a relative basis. For now, the easy money trade is back at the fore and everything else is taking a back seat.

Monday-Wednesday’s Action: All Eyes On The Fed

Stocks edged lower on Monday as investors digested a very strong four-week rally. New Home Sales hit an annualized rate of 468k units in September, missing estimates for 550k. It also missed August’s rate of 529k. Stocks slid on Tuesday as the Fed began their October meeting. Before the open, durable goods slid by -1.2%, missing estimates for -1.0%. The Case-Shiller Index rose by 0.1%, matching estimates for 0.1%. The PMI service flash index came in at 54.4, missing estimates for 55.3. Consumer confidence came in at 97.6, missing estimates for 102.5. The Richmond Fed Manufacturing index slid to -1, barely beating estimates for -2. In other news, oil prices continued to slide on supply woes. Stocks soared on Wednesday after the Fed held its latest meeting and decided to keep rates unchanged near zero. That gave the green light that the very powerful easy money trade is alive and well. Shares of Apple (AAPL) rallied after reporting their latest quarterly results. Shares of Twitter (TWTR) fell sharply after releasing earnings.

Thursday-Friday’s Action: Easy Money Sends Stocks Higher..Again

Stocks edged lower on Thursday after the government said Q3 GDP rose by +1.5%, missing estimates for +1.6%. This was the latest in a series of weaker than expected economic results and reiterated our thesis that Main Street is simply not ready for a rate hike (even though Wall Street is). Elsewhere, weekly initial claims level rose to 260k, beating estimates for 264k. After Thursday’s close, shares of LinkedIn (LNKD) rallied after releasing earnings. Stocks were quiet on Friday as investors digested very strong monthly gains on the last trading day of the month..

Market Outlook: Bulls Are Strong

This bull market is aging by any normal definition and will celebrate its 7th anniversary in March 2015. The last two major bull markets ended shortly after their 5th anniversary; 1994-2000 & 2002-Oct 2007. The fact that easy money is here to stay (for now) is all that matters. Everything else is noise. Eventually that will change, but for now the bulls remain in control. As always, keep your losses small and never argue with the tape. If you want exact entry and exit points in leading stocks, or access more of Adam’s commentary/thoughts on the market – Join FindLeadingStocks.com.

The Nasdaq and the S&P 500 traded in a range before closing near their session lows of 4,836.46 and 2,017.22.

S&P 500 intraday

The Dow Jones industrial average was also in a range, and nearly rose 100 points as Boeing pushed the blue chips index higher after reporting better-than-expected earnings.

Dow Jones industrial average intraday

“The story in the Dow is United Technologies and Boeing versus UnitedHealth Group and Goldman Sachs,” said Art Hogan, chief market strategist at Wunderlich Securities.

United Technologies closed up 2.46 percent, while Boeing ended 1.66 percent higher. Goldman closed down 3.13 percent and UnitedHealthfell 1.92 percent.

Read MoreLatest IBM miss another $600M hit to Warren Buffett

Other companies that posted quarterly results Wednesday includedCoca-Cola and General Motors. GM beat expectations on both earnings and revenue, but Coca-Cola sales fell short of estimates.

“Overall, we seem to be running at the same pace we’ve been running at the last few quarters,” said Randy Frederick, managing director of trading and derivatives at Charles Schwab.

Shares of GM rose closed up 5.79 percent after rising over 6.5 percent, while Coca-Cola’s stock traded slightly lower.

“That doesn’t take away that only 44 percent of companies have beaten on revenues,” said Nick Raich, CEO of The Earnings Scout.

Read MoreTop managers give under-the-radar earnings picks

Firms scheduled to report after the bell include American Express,eBay and Raymond James.

“We’ve had some pretty rocky earnings, and volatility has been pretty much contained,” said Peter Cardillo, chief market economist at Rockwell Global Capital.

“With all these individual stock stories, the indexes are hanging in pretty nicely,” Hogan said.

On Tuesday, stocks closed narrowly lower as IBM posted disappointing earnings.

Stock took a hit Wednesday as health care turned negative year-to-date.

“Valeant is the killer,,” said Howard Silverblatt, senior index analyst at S&P Dow Jones Indices.

Valeant Pharmaceuticals plunged as much as 28 percent after the release of a short-seller note on the company.

“Now they’re comparing it to Enron,” Silverblatt said.

Read MoreDon’t look now, but bonds are back (junk, too)

Valeant stock intraday

Investors also digested EIA oil inventories data, which showed inventories rise by 8 million barrels, as U.S. crude prices have fallen over 4.5 percent this week.

U.S. oil futures closed down 2.4 percent at $45.20 a barrel, posting their third straight day of losses.

“We think about low oil as being good for the economy, but I think it’s gotten too low and it’s become a drag in the economy,” Frederick said.

Read MoreTokyo jumps, but Shanghai posts biggest fall in 5 weeks

Wall Street also digested Japanese exports data, which came in far weaker than expected. Japan’s annual export growth slowed for the third straight month in September, raising questions as to whether or not the Bank of Japan will go further into its qualitative and quantitative easing program.

The data prodded up the Nikkei 225, which closed up nearly 2 percent, while China’s Shanghai Composite tumbled 3.47 percent.

“Big picture, easy money is here to stay,” said Adam Sarhan, CEO of Sarhan Capital.

U.S. Treasurys gained ground, as the 10-year yield fell to 2.02 percent and the two-year yielded 0.61 percent.

In Europe, stocks ended mixed, with the pan-European STOXX 600 closing flat and the German DAX ending higher in anticipation of Thursday’s European Central Bank meeting.

In corporate news, Ferrari closed up 5.77 percent at $55 a share on itsfirst day of trading.

SanDisk will be bought by Western Digital for $86.50 a share in cash and stock, or $19 billion.

Morgan Stanley downgraded Twitter‘s stock to “underweight” from “equal-weight,” citing limited user growth and a lack of advertiser demand growth.

Toyota will recall 6.5 million vehicles to fix a power window defect, and another 2 million will be recalled for a potential fire hazard.

The Dow Jones industrial average closed down 48.50 points, or 0.28 percent, to 17,168.60, led lower by Glodman Sachs and with United Technologies leading advancers.

The S&P 500 ended 11.83 points lower, or 0.58 percent at 2,018.94, with energy leading nine sectors lower and industrials the only advancer.

The Nasdaq closed 40.85 points lower, or 0.84 percent, to 4,840.12.

Gold futures settled down $10.40 at $1,167.10 an ounce.

The dollar traded slightly higher against a basket of major currencies.

Decliners led advancers 3 to 1 at the New York Stock Exchange, with an exchange volume of 852 million and a composite volume of 3.591 billion at the close.